![]()

Afterword: The Descent of Moneyfrom The Ascent of Money (Amazon) by Niall Ferguson Today’s financial world is the result of four millennia of economic evolution. Money — the crystallized relationship between debtor and creditor begat banks, clearing houses for ever larger aggregations of borrowing and lending. From the thirteenth century onwards, government bonds introduced the securitization of streams of interest payments; while bond markets revealed the benefits of regulated public markets for trading and pricing securities. From the seventeenth century, equity in corporations could be bought and sold in similar ways. From the eighteenth century, insurance funds and then pension funds exploited economies of scale and the laws of averages to provide financial protection against calculable risk. From the nineteenth, futures and options offered more specialized and sophisticated instruments: the first derivatives. And, from the twentieth, households were encouraged, for political reasons, to increase leverage and skew their portfolios in favor of real estate. Economies that combined all these institutional innovations banks, bond markets, stock markets, insurance and property-owning democracy performed better over the long run than those that did not, because financial intermediation generally permits a more efficient allocation of resources than, say, feudalism or central planning. For this reason,it is not wholly surprising that the Western financial model tended to spread around the world, first in the guise of imperialism, then in the guise of globalization.’ From ancient Mesopotamia to present-day China, in short, the ascent of money has been one of the driving forces behind human progress: a complex process of innovation, intermediation and integration that has been as vital as the advance of science or the spread of law in mankind’s escape from the drudgery of subsistence agriculture and the misery of the Malthusian trap. [Malthusianism is the idea that population growth is potentially exponential while the growth of the food supply or other resources is linear.](https://en.wikipedia.org/wiki/Malthusianism) In the words of former Federal Reserve Governor Frederic Mishkin, ‘the financial system [is] the brain of the economy … It acts as a coordinating mechanism that allocates capital, the lifeblood of economic activity, to its most productive uses by businesses and households. If capital goes to the wrong uses or does not flow at all, the economy will operate inefficiently, and ultimately economic growth will be low.’ Yet money’s ascent has not been, and can never be, a smooth one. On the contrary, financial history is a roller-coaster ride of ups and downs, bubbles and busts, manias and panics, shocks and crashes. One recent study of the available data for gross domestic product and consumption since 1870 has identified 148 crises in which a country experienced a cumulative decline in GDP of at least 10 per cent and eighty-seven crises in which consumption suffered a fall of comparable magnitude, implying a probability of financial disaster of around 3.6 per cent per year. Even today, despite the unprecedented sophistication of our institutions and instruments, Planet Finance remains as vulnerable as ever to crises. It seems that, for all our ingenuity, we are doomed to be “fooled by randomness” and surprised by ‘black swans’. It may even be that we are living through the deflation of a multi-decade ‘super bubble’.? There are three fundamental reasons for this. The first is that so much about the future — or, rather, futureS, since there is never a singular future — lies in the realm of uncertainty, as opposed to calculable risk. As Frank Knight argued in 1921, uncertainty must be taken in a sense radically distinct from the familiar notion of risk, from which it has never been properly separated. A measurable uncertainty, or “risk” proper is so far different from an unmeasurable one that it is not in effect an uncertainty at all.’ To put it simply, much of what happens in life isn’t like game of dice. Again and again an event will occur that is ‘so entirely unique that there are no others or not a sufficient number to make it possible to tabulate enough like it to form a basis for any inference of value about any real probability … The same point was brilliantly expressed by Keynes in I937. ‘By “uncertain” knowledge,’ he wrote in a response to critics of his General Theory, … I do not mean merely to distinguish what is known for certain from what is only probable. The game of roulette is not subject, in this sense, to uncertainty The expectation of life is only slightly uncertain. Even the weather is only moderately uncertain. The sense in which I am using the term is that in which the prospect of a European war is uncertain, or ., the rate of interest twenty years hence … About these matters there is no scientific basis on which to form any calculable probability whatever. We simply do not know.* As Peter Bernstein has said, ‘We pour in data from the past but past data constitute a sequence of events rather than a set of independent observations, which is what the laws of probability demand. History provides us with only one sample of the … capital markets, not with thousands of separate and randomly distributed numbers.’ The same problem — that the sample size is effectively on is of course inherent in geology, a more advanced historical science than financial history, as Larry Neal has observed. Keynes went on to hypothesize about the ways in which investors ‘manage in such circumstances to behave in a manner which saves our faces as rational, economic men’: (1) We assume that the present is a much more serviceable guide to the future than candid examination of past experience would show it to have been hitherto. In other words we largely ignore the prospect of future changes about the actual character of which we know nothing. (2) We assume that the existing state of opinion as expressed in prices and the character of existing output is based on a correct summing up of future prospects … (3) Knowing that our own individual judgment is worthless, we endeavor to fall back on the judgment of the rest of the world which is perhaps better informed. That is, we endeavor to conform with the behavior of the majority or the average.’ Though it is far from clear that Keynes was correct in his interpretation of investors’ behavior, he was certainly thinking along the right lines. For there is no question that the heuristic biases of individuals play a critical role in generating volatility in financial markets. This brings us to the second reason for the inherent instability of the financial system: human behavior. As we have seen, all financial institutions are at the mercy of our innate inclination to veer from euphoria to despondency; our recurrent inability to protect ourselves against ‘tail risk’; our perennial failure to learn from history. Tail risk is a form of portfolio risk that arises when the possibility that an investment will move more than three standard deviations from the mean is greater than what is shown by a normal distribution In a famous article, Daniel Kahneman and Amos Tversky demonstrated with a series of experiments the tendency that people have to miscalculate probabilities when confronted with simple financial choices. First, they gave their sample group 1,000 Israeli pounds each. Then they offered them a choice between either a) a 50 per cent chance of winning an additional 1,000 pounds or b) 100 per cent chance of winning an additional 500 pounds. Only 16 per cent of people chose a); everyone else (84 per cent) chose b). Next, they asked the same group to imagine having received 2,000 Israeli pounds each and confronted them with another choice: between either c) a 50 per cent chance of losing 1,000 pounds or b) a 100 per cent chance of losing 500 pounds. This time the majority (69 per cent) chose a); only 31 per cent chose b). Yet, viewed in terms of their payoffs, the two problems are identical. In both cases you have a choice between a 50 per cent chance of ending up with 1,000 pounds and an equal chance of ending up with 2,000 pounds (a and c) or a certainty of ending up with 1,500 pounds (b and d). In this and other experiments, Kahneman and Tversky identify a striking asymmetry: risk aversion for positive prospects, but risk seeking for negative ones. A loss has about two and a half times the impact of a gain of the same magnitude. This ‘failure of invariance’ is only one of many heuristic biases (skewed modes of thinking or learning) that distinguish real human beings from the homo oeconomicus of neoclassical economic theory, who is supposed to make his decisions rationally, on the basis of all the available information and his expected utility. Other experiments show that we also succumb too readily to such cognitive traps as: Availability bias, which causes us to base decisions on information that is more readily available in our memories, rather than the data we really need; Hindsight bias, which causes us to attach higher probabilities to events after they have happened (ex post) than we did before they happened (ex ante); The problem of induction, which leads us to formulate general rules on the basis of insufficient information; The fallacy of conjunction (or disjunction), which means we tend to overestimate the probability that seven events of 90 per cent probability will all occur, while underestimating the probability that at least one of seven events of 10 per cent probability will occur; Confirmation bias, which inclines us to look for confirming evidence of an initial hypothesis, rather than falsifying evidence that would disprove it; Contamination effects, whereby we allow irrelevant but proximate information to influence a decision; The affect heuristic, whereby preconceived value-judgements interfere with our assessment of costs and benefits; Scope neglect, which prevents us from proportionately adjusting what we should be willing to sacrifice to avoid harms of different orders of magnitude; Overconfidence in calibration, which leads us to underestimate the confidence intervals within which our estimates will be robust (e.g. to conflate the best case’ scenario with the ʻmost probable’); and Bystander apathy, which inclines us to abdicate individual responsibility when in a crowd. If you still doubt the hard-wired fallibility of human beings, yourself the following question. A bat and ball, together, cost a total of 1.10 and the bat costs £I more than the ball. How much is the ball? The wrong answer is the one that roughly one in every two people blurts out: 10 pence. The correct answer is 5 pence, since only with a bat worth 1.05 and a ball worth 5 pence are both conditions satisfied If any field has the potential to revolutionize our understanding of the way financial markets work, it must surely be the burgeoning discipline of behavioral finance. It is far from clear how much of the body of work derived from the efficient markets hypothesis can survive this challenge. Those who put their faith in the ‘wisdom of crowds’ mean no more than that a large group of people is more likely to make a correct assessment than a small group of supposed experts. But that is not saying much. The old joke that ‘Macroeconomists have successfully predicted nine of the last five recessions is not so much a joke as a dispiriting truth about the difficulty of economic forecasting. Meanwhile, serious students of human psychology will expect as much madness as wisdom from large groups of people.” A case in point must be the near-universal delusion among investors in the first half of 2007 that a major liquidity crisis could not occur (see Introduction). To adapt an elegant summation by Eliezer Yudkowsky: People may be overconfident and over-optimistic. They may focus on overly specific scenarios for the future, to the exclusion of all others. They may not recall any past liquidity crises] in memory. They may overestimate the predictability of the past, and hence underestimate the surprise of the future. They may not realize the difficulty of preparing for [liquidity crises] without the benefit of hindsight. They may prefer … gambles with higher payoff probabilities, neglecting the value of the stakes. They may conflate positive information about the benefits of a technology [e-g.bond insurance] and negative information about its risks. They may be contaminated by movies where the [financial system] ends up being saved … Or the extremely unpleasant prospect of [a liquidity crisis] may spur them to seek arguments that [liquidity] will not [dry up], without an equally frantic search for reasons why [it should]. But if the question is, specifically, “Why aren’t more people doing something about it?’, one possible component is that people are asking that very question — darting their eyes around to see if anyone else is reacting … meanwhile trying to appear poised and unflustered. Most of our cognitive warping is, of course, the result of evolution. The third reason for the erratic path of financial history is also related to the theory of evolution, though by analogy. It is commonly said that finance has a Darwinian quality. “The survival of the fittest’ is a phrase that aggressive traders like to use; as we have seen, investment banks like to hold conferences with titles like ‘The Evolution of Excellence’. But the American crisis of 2007 has increased the frequency of such language. US Assistant Secretary of the Treasury Anthony W. Ryan was not the only person to talk in terms of a wave of financial extinctions in the second half of 2007. Andrew Lo, director of the Massachusetts Institute of Technology’s Laboratory for Financial Engineering, is in the vanguard of an effort to re-conceptualize markets as adaptive systems. A long-run historical analysis of the development of financial services also suggests that evolutionary forces are present in the financial world as much as they are in the natural world. The notion that Darwinian processes may be at work in the economy is not new, of course. Evolutionary economics is in fact a well-established sub-discipline, which has had its own dedicated journal for the past sixteen years.

Thorstein Veblen first posed the question ‘Why is Economics Not an Evolutionary Science?’ (implying that it really should be) as long ago as 1898. Nor is this evolutionary character due to quasi-autonomic increase in population and capital or to the vagaries of monetary systems of which exactly the same thing holds true. The fundamental impulse that sets and keeps the capitalist engine in motion comes from the new consumers’ goods, the new methods of production or transportation, the new markets, the new forms of industrial organization that capitalist enterprise creates … The opening up of new markets, foreign or domestic, and the organizational development from the craft shop and factory to such concerns as US Steel illustrate the same process of industrial mutation — if may use the biological term — that incessantly revolutionizes the economic structure from within, incessantly destroying the old one, incessantly creating a new one. This process of Creative Destruction is the essential fact about capitalism. A key point that emerges from recent research is just how much destruction goes on in a modern economy. Around one in ten US companies disappears each year. Between 1989 and 1997, to be precise, an average of 611,000 businesses a year vanished out of a total of 5.73 million firms. Ten per cent is the average extinction rate, it should be noted; in some sectors of the economy it can rise as high as 20 per cent in a bad year (as in the District of Columbia’s financial sector in 1989, at the height of the Savings and Loans crisis). According to the UK Department of Trade and Industry, 30 per cent of tax-registered businesses disappear after three years. Even if they survive the first few years of existence and go on to enjoy great success, most firms fail eventually. Of the world’s 100 largest companies in 1912, 29 were bankrupt by 1995, 48 had disappeared, and only 19 were still in the top 100. Given that a good deal of what banks and stock markets do is to provide finance to companies, we should not be surprised to find a similar pattern of creative destruction in the financial world. We have already noted the high attrition rate among hedge funds. (The only reason that more banks do not fail, as we shall see, is that they are explicitly and implicitly protected from collapse by governments.) What are the common features shared by the financial world and a true evolutionary system? Six spring to mind: ‘Genes’, in the sense that certain business practices perform the same role as genes in biology, allowing information to be stored in the ‘organizational memory’ and passed on from individual to individual or from firm to firm when a new firm is created. The potential for spontaneous mutation, usually referred to in the economic world as innovation and primarily, though by no means always, technological. Competition between individuals within a species for resources, with the outcomes in terms of longevity and proliferation determining which business practices persist. A mechanism for natural selection through the market allocation of capital and human resources and the possibility of death in cases of under-performance, i.e. ‘differential survival’. Scope for speciation, sustaining biodiversity through the creation of wholly new species of financial institutions. Scope for extinction, with species dying out altogether. Financial history is essentially the result of institutional mutation and natural selection. Random ‘drift’ (innovations/ mutations that are not promoted by natural selection, but just happen) and ‘flow’ (innovations/mutations that are caused when, say, American practices are adopted by Chinese banks) play a part. There can also be ‘co-evolution’, when different financial species work and adapt together (like hedge funds and their prime brokers). But market selection is the main driver. Financial organisms are in competition with one another for finite resources. At certain times and in certain places, certain species may become dominant. But innovations by competitor species, or the emergence of altogether new species, prevent any permanent hierarchy or monoculture from emerging. Broadly speaking, the law of the survival of the fittest applies. Institutions with a ‘selfish gene’ that is good at self-replication and self-perpetuation will tend to proliferate and endure. Note that this may not result in the evolution of the perfect organism. A ‘good enough’ mutation will achieve dominance if it happens in the right place at the right time, because of the sensitivity of the evolutionary process to initial conditions; that is, an initial slim advantage may translate into a prolonged period of dominance, without necessarily being optimal. It is also worth bearing in mind that in the natural world, evolution is not progressive, as used to be thought (notably by the followers of Herbert Spencer). Primitive financial life-forms like loan sharks are not condemned to oblivion, any more than the microscopic prokaryotes that still account for the majority of earth’s species. Evolved complexity protects neither an organism nor a firm against extinction — the fate of most animal and plant species. The evolutionary analogy is, admittedly, imperfect. When one organism ingests another in the natural world, it is just eating; whereas, in the world of financial services, mergers and acquisitions can lead directly to mutation. Among financial organisms, there is no counterpart to the role of sexual reproduction in the animal world (though demotic sexual language is often used to describe certain kinds of financial transaction). Most financial mutation is deliberate, conscious innovation, rather than random change. Indeed, because a firm can adapt within its own lifetime to change going on around it, financial evolution (like cultural evolution) may be more Lamarckian than Darwinian in character. Two other key differences will be discussed below. Nevertheless, evolution certainly offers a better model for understanding financial change than any other we have. Ninety years ago, the German socialist Rudolf Hilferding predicted an inexorable movement towards more concentration of ownership in what he termed finance capital. The conventional view of financial development does indeed see the process from the vantage point of the big, successful survivor firm. In Citigroup’s official family tree, numerous small firms — dating back to the City Bank of New York, founded in 1812 — are seen to converge over time on a common trunk, the present-day conglomerate. However, this is precisely the wrong way to think about financial evolution over the long run, which begins at a common trunk. Periodically, the trunk branches outwards as new kinds of bank and other financial institution evolve. The fact that a particular firm successfully devours smaller firms along the way is more or less irrelevant. In the evolutionary process, animals eat one another, but that is not the driving force behind evolutionary mutation and the emergence of new species and sub-species. The point is that economies of scale and scope are not always the driving force in financial history. More often, the real drivers are the process of speciation whereby entirely new types of firm are created — and the equally recurrent process of creative destruction, whereby weaker firms die out. Take the case of retail and commercial banking, where there remains considerable biodiversity. Although giants like Citigroup and Bank of America exist, North America and some European markets still have relatively fragmented retail banking sectors. The cooperative banking sector has seen the most change in recent years, with high levels of consolidation (especially following the Savings and Loans crisis of the 1980s), and most institutions moving to shareholder ownership. But the only species that is now close to extinction in the developed world is the state-owned bank, as privatization has swept the world (though the nationalization of Northern Rock suggests the species could make a comeback). In other respects, the story is one of speciation, the proliferation of new types of financial institution, which is just what we would expect in a truly evolutionary system. Many new ‘mono-line’ financial services firms have emerged, especially in consumer finance (for example, Capital One). A number of new ‘boutiques’ now exist to cater to the private banking market. Direct banking (telephone and Internet) is another relatively recent and growing phenomenon. Likewise, even as giants have formed in the realm of investment banking, new and nimbler species such as hedge funds and private equity partnerships have evolved and proliferated. And, as we saw in Chapter 6, the rapidly accruing hard currency reserves of exporters of manufactured goods and energy are producing a new generation of sovereign wealth funds. Not only are new forms of financial firm proliferating; so too are new forms of financial asset and service. In recent years, investors’ appetite has grown dramatically for mortgage-backed and other asset-backed securities. The use of derivatives has also increased enormously, with the majority being bought and sold ‘over the counter’, on a one-to-one bespoke basis, rather than a through public exchanges — tendency which, though profitable for the sellers of derivatives, may have unpleasant as well as unintended consequences because of the lack of standardization of these instruments and the potential for legal disputes in the event of a crisis. In evolutionary terms, then, the financial services sector appears to have passed through a a twenty-year Cambrian explosion, with existing species flourishing and new species increasing in number. As in the natural world, the existence of giants has not precluded the evolution and continued existence of smaller species. Size isn’t everything, in finance as in nature. Indeed, the very difficulties that arise as publicly owned firms become larger and more complex — the diseconomies of scale associated with bureaucracy, the pressures associated with quarterly reporting give opportunities to new forms of private firm. What matters in evolution is not your size or (beyond a certain level) your complexity. All that matters is that you are good at surviving and reproducing your genes. The financial equivalent is being good at generating returns on equity and generating imitators employing a similar business model. In the financial world, mutation and speciation have usually been evolved responses to the environment and competition, with natural selection determining which new traits become widely disseminated. Sometimes, as in the natural world, the evolutionary process has been subject to big disruptions in the form of geopolitical shocks and financial crises. The difference is, of course, that whereas giant asteroids (like the one that eliminated 85 per cent of species at the end of the Cretaceous period) are exogenous shocks, financial crises are endogenous to the financial system. The Great Depression of the 1930s and the Great Inflation of the 1970s stand out as times of major discontinuity, with ‘mass extinctions’ such as the bank panics of the 1930s and the Savings and Loans failures of the 1980s. Could something similar be happening in our time? Certainly, the sharp deterioration in credit conditions in the summer of 2007 created acute problems for many hedge funds, leaving them vulnerable to redemptions by investors. But a more important feature of the recent credit crunch has been the pressure on banks and insurance companies. Losses on asset-backed securities and other forms of risky debt are thought likely to be in excess of $1 trillion. At the time of writing (May 2008), around $318 billion of write-downs (booked losses) have been acknowledged, which means that more than $600 billion of losses have yet to come to light. Since the onset of the crisis, financial institutions have raised around $225 billion of new capital, leaving a shortfall of slightly less than $100 billion. Since banks typically target a constant capital/assets ratio of less than 10 per cent, that implies that balance sheets may need to be shrunk by as much as $1 trillion. However, the collapse of the so-called shadow banking system of off-balance-sheet entities such as structured investment vehicles and conduits is making that contraction very difficult indeed. It remains to be seen whether the major Western banks can navigate their way through this crisis without a fundamental change to the international accords (Basel I and II)* governing capital adequacy. Under the Basel I rules agreed in 1988, assets of banks are divided into five categories according to credit risk, carrying risk weights ranging from zero (for example, home country government bonds) to 100 per cent (corporate debt). International banks are required to hold capital equal to 8 per cent of their risk-weighted assets. Basel II, first published in 2004 but only gradually being adopted around the world, sets out more complex rules, distinguishing between credit risk, operational risk and market risk, the last of which mandates the use of value at risk (VaR) models. Ironically, in the light of 2007-8, liquidity risk is combined with other risks under the heading ‘residual risk’. Such rules inevitably conflict with the incentive all banks have to minimize their capital and hence raise their return on equity. In Europe, for example, average bank capital is now equivalent to significantly less than 10 per cent of assets (perhaps as little as 4) compared with around 25 per cent towards the beginning of the twentieth century. The 2007 crisis has dashed the hopes of those who believed that the separation of risk origination and balance sheet management would distribute risk optimally throughout the financial system. It seems inconceivable that this crisis will pass without further mergers and acquisitions, as the relatively strong devour the relatively weak. Bond insurance companies seem destined to disappear. Some hedge funds, by contrast, are likely to thrive on the return of volatility.* In Andrew Lo’s words: ‘Hedge funds are the Galapagos Islands of finance The rate of innovation, evolution, competition, adaptation, births and deaths, the whole range of evolutionary phenomena, occurs at an extraordinarily rapid clip.’ It also seems likely that new forms of financial institution will spring up in the aftermath of the crisis. As Andrew Lo has suggested; As with past forest fires in the markets, we’re likely to see incredible flora and fauna springing up in its wake.’ There is another big difference between nature and finance Whereas evolution in biology takes place in the natural environment, where change is essentially random (hence Richard Dawkins’s image of the blind watchmaker), evolution in financial services occurs within a regulatory framework where — to borrow a phrase from anti-Darwinian creationists ‘intelligent design’ plays part. Sudden changes to the regulatory environment are rather different from sudden changes in the macroeconomic environment, which are analogous to environmental changes in the natural world. The difference is once again that there is an element of endogeneity in regulatory changes, since those responsible are often poachers turned gamekeepers, with good insight into the way that the private sector works. The net effect, however, is similar to climate change on biological evolution. New rules and regulations can make previously good traits suddenly disadvantageous. The rise and fall of Savings and Loans, for example, was due in large measure to changes in the regulatory environment in the United States. Regulatory changes in the wake of the 2007 crisis may have comparably unforeseen consequences. The stated intention of most regulators is to maintain stability within the financial services sector, thereby protecting the consumers whom banks serve and the ‘real’ economy which the industry supports. Companies in non-financial industries are seen as less systemically important to the economy as a whole and less critical to the livelihood of the consumer. The collapse of a major financial institution, in which retail customers lose their deposits, is therefore an event which any regulator (and politician) wishes to avoid at all costs. An old question that has raised its head since August 2007 is how far implicit guarantees to bail out banks create a a problem of moral hazard, encouraging excessive risk-taking on the assumption that the state will intervene to avert illiquidity and even insolvency if an institution is considered too big to fail meaning too politically sensitive or too likely to bring a lot of other firms down with it. From an evolutionary perspective, however, the problem looks slightly different. It may, in fact, be undesirable to have any institutions in the category of ‘too big to fail’, because without occasional bouts of creative destruction the evolutionary process will be thwarted. The experience of Japan in the 1990s stands as a warning to legislators and regulators that an entire banking sector can become a kind of economic dead hand if institutions are propped up despite underperformance, and bad debts are not written off. Every shock to the financial system must result in casualties. Left to itself, natural selection should work fast to eliminate the weakest institutions in the market, which typically are gobbled up by the successful. But most crises also usher in new rules and regulations, as legislators and regulators rush to stabilize the financial system and to protect the consumer/voter. The critical point is that the possibility of extinction cannot and should not be removed by excessively precautionary rules. As Joseph Schumpeter wrote more than seventy years ago, ‘This economic system cannot do without the ultima ratio of the complete destruction of those existences which are irretrievably associated with the hopelessly unadapted.’ This meant, in his view, nothing less than the disappearance of ‘those firms which are unfit to live.’ In writing this book, I have frequently been asked if I gave it the wrong title. The Ascent of Money may seem to sound an incongruously optimistic note (especially to those who miss the allusion to Bronowski’s Ascent of Man) at a time when a surge of inflation and a flight into commodities seem to signal a literal descent in public esteem and purchasing power of fiat moneys like the dollar. Yet it should by now be obvious to the reader just how far our financial system has ascended since its distant origins among the moneylenders of Mesopotamia. There have been great reverses, contractions and dyings, to be sure. But not even the worst has set us permanently back. Though the line of financial history has a saw-tooth quality, its trajectory is unquestionably upwards. Still, I might equally well have paid homage to Charles Darwin by calling the book The Descent of Finance, for the story I have told is authentically evolutionary. When we withdraw banknotes from automated telling machines, or invest portions of our monthly salaries in bonds and stocks, or insure our cars, or remortgage our homes, or renounce home bias in favor of emerging markets, we are entering into transactions with many historical antecedents. I remain more than ever convinced that, until we fully understand the origin of financial species, we shall never understand the fundamental truth about money: that, far from being ‘a monster that must be put back in its place’, as the German president recently complained,” financial markets are like the mirror of mankind, revealing every hour of every working day the way we value ourselves and the resources of the world around us. It is not the fault of the mirror if it reflects our blemishes as clearly as our beauty. |

|

“The greatest danger in times of turbulence is not turbulence; it is to act with yesterday’s logic”. — Peter Drucker The shift from manual workers who do as they are being told — either by the task or by the boss — to knowledge workers who have to manage themselves ↓ profoundly challenges social structure …

“Managing Oneself (PDF) is a REVOLUTION in human affairs.” … “It also requires an almost 180-degree change in the knowledge workers’ thoughts and actions from what most of us—even of the younger generation—still take for granted as the way to think and the way to act.” …

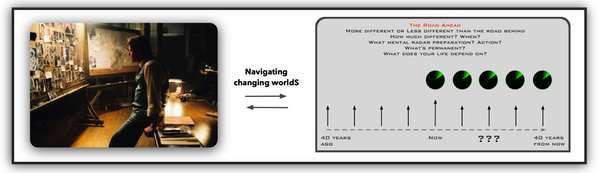

These pages are attention directing tools for navigating a world moving relentlessly toward unimagined futures.

What’s the next effective action on the road ahead

It’s up to you to figure out what to harvest and calendarize It may be a step forward to actively reject something (rather than just passively ignoring) and then working out a plan for coping with what you’ve rejected. Your future is between your ears and our future is between our collective ears — it can’t be otherwise. A site exploration starting point → The memo THEY don't want you to see

To create a rlaexp.com site search, go to Google’s site ↓ Type the following in their search box ↓ your search text site:rlaexp.com

Copyright 1985 through 2020 © All rights reserved | bobembry | bob embry | “time life navigation” © #TimeLifeNavigation | “life TIME investment system” © #LifeTimeInvestmentSystem | “career evolution” © #CareerEvolution | “life design” © #LifeDesign | “organization evolution” © #OrganizationEvolution | “brainroads toward tomorrows” © #BrainroadsTowardTomorrows | “foundations for future directed decisions” © #FoundationsForFutureDirectedDecisions | #rlaexpdotcom © | rlaexpdotcom © rlaexp.com = rla + exp = real life adventures + exploration or explored exploration leads to explored Examples ↑ can be found through web searches, Wikipedia #rlaexpdotcom introduction breadcrumb trail … |